DISCLAIMER: GoldInvestors.news is not a registered investment, legal or tax advisor or broker/dealer. All investment/financial opinions expressed by GoldInvestors.news are from the personal research and experience of the owner of the site and are intended as educational material. Although best efforts are made to ensure that all information is accurate and up to date, occasionally unintended errors and misprints may occur.

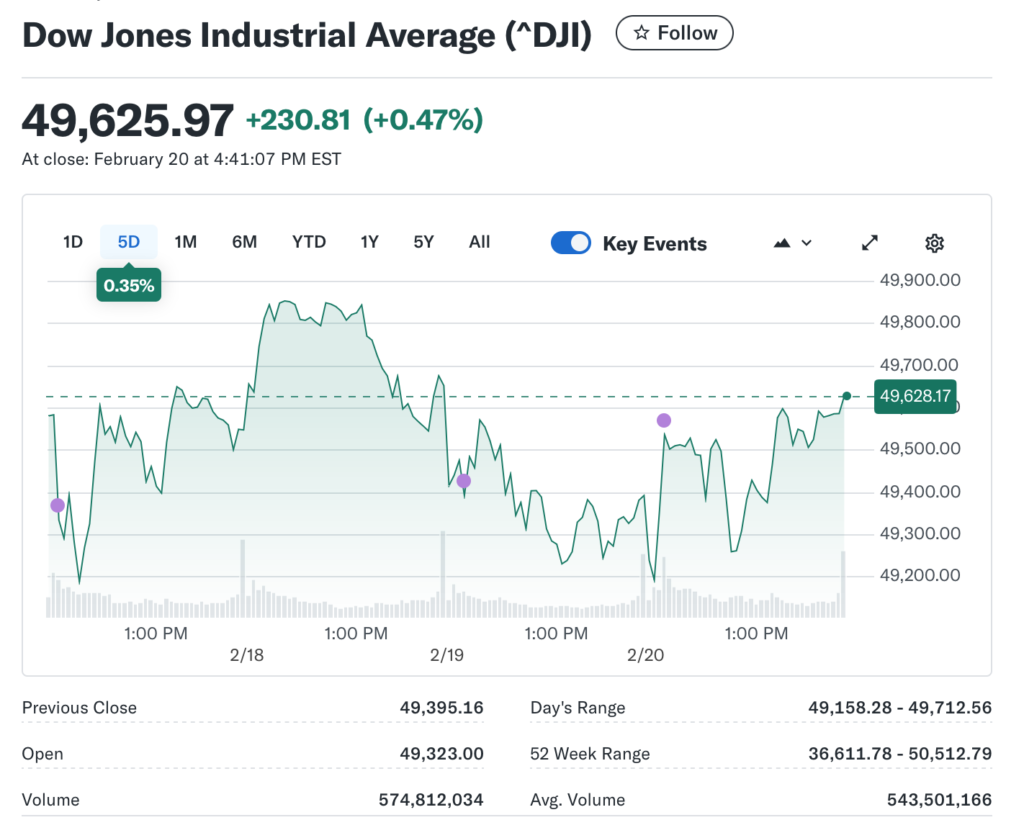

Stock markets rarely move in a straight line, and yesterday proved that again as buyers stepped in at session close, lifting major indices and offsetting early softness amid a delicate balance of optimism and caution.

The day featured headlines that spanned encouragement and concern, signaling that a comeback can take root even amid mixed signals and the growing realization that sector leadership will be selective and data dependent.

Here's What They're Not Telling You About Your Retirement

From a policy and profitability standpoint the backdrop remains complex, yet several undercurrents supported higher prices as investors sifted through corporate results, central bank commentary, and evolving macro signals.

Surging corporate earnings in pivotal sectors, cooling inflation data, and modest relief from supply chain bottlenecks gave traders confidence that the economy can expand without reigniting price pressures while policymakers debate the pace of normalization.

Investors also weighed the trajectory of monetary policy, betting that rate normalization or gradual cuts may be on the horizon and that a more predictable path could reduce uncertainty for long term valuations.

That view helped steady equity multiples and encouraged risk-taking, even as debt concerns and leverage in parts of the economy remained a talking point that could shift suddenly if growth surprises to the upside or downside.

This Could Be the Most Important Video Gun Owners Watch All Year

Sector composition reflected a rotation toward assets viewed as better positioned to weather uncertainty in a slower growth environment and a climate of policymaker caution.

Tech leaders, financially sound cyclicals, and selective defensive names traded at premiums that some argue are justified by earnings resilience while others worry about overextension in an uncertain macro climate.

The market’s mood has been shaped by a steady stream of headlines that mix good news with cautionary tales, inviting traders to reassess risk every few hours.

Despite robust consumer spending and resilient earnings, concerns about geopolitics, energy markets, and debt dynamics kept volatility elevated and reminded investors that no rally is built on a single pillar.

For many, the episode underscored the need for disciplined risk management and diversification across asset classes, geographies, and time horizons. Gold and other traditional hedges remained part of the toolkit, not as a speculative bet but as a structural ballast against the known uncertainties that come with policy transition and economic cycles.

Folded into the price action was a careful calibration between bonds and stocks, with yields oscillating in response to new data and Fed guidance while investors weighed the tradeoffs of duration, credit risk, and liquidity.

When rates priced in a slower trajectory, equities tended to rally in modest fashion, while tougher data or hawkish pivots tended to pause or reverse progress and force a reallocation toward smoother growth narratives.

Longer term, the macro landscape remains a test of decades of debt, demographics, and productivity dynamics, a framework that argues for caution despite occasional optimism.

That backdrop does not vanish with a quarterly rally, which is why investors balance near term gains against structural headwinds that could reassert themselves as policy normalizes and fiscal impulses ebb.

Sentiment can move markets as much as fundamentals, and fear of missing out often fuels late bout of buying when headlines momentarily tilt toward optimism.

At the same time, rational analysis about risk, return, and capital preservation anchors decisions even during bouts of optimism, reminding investors to separate narrative from data.

Economic data releases in coming weeks will test whether the rally can convert into sustainable gains, particularly if inflation stubbornly sticks or employment trends surprise to the upside.

Inflation readings, employment reports, and corporate earnings will influence expectations for rate paths and sector leadership, shaping the next leg higher or a period of consolidation as investors recalibrate.

Investors should not mistake a rebound for a permanent shift in trend, since markets tend to reprice after disappointment and surprise.

Volatility is likely to persist as the economy digests policy shifts, earnings revisions, and geopolitical headlines that never truly disappear, keeping risk management front and center.

In a cautious but opportunistic market, patience and discipline remain the investor’s best allies, guiding capital toward durable franchises and time tested strategies.

The comeback story is real, but it will test conviction, not give it away, demanding judgment that blends prudence with readiness to act when conditions align.

DISCLAIMER: GoldInvestors.news is not a registered investment, legal or tax advisor or broker/dealer. All investment/financial opinions expressed by GoldInvestors.news are from the personal research and experience of the owner of the site and are intended as educational material. Although best efforts are made to ensure that all information is accurate and up to date, occasionally unintended errors and misprints may occur.

Join the Discussion

COMMENTS POLICY: We have no tolerance for messages of violence, racism, vulgarity, obscenity or other such discourteous behavior. Thank you for contributing to a respectful and useful online dialogue.