DISCLAIMER: GoldInvestors.news is not a registered investment, legal or tax advisor or broker/dealer. All investment/financial opinions expressed by GoldInvestors.news are from the personal research and experience of the owner of the site and are intended as educational material. Although best efforts are made to ensure that all information is accurate and up to date, occasionally unintended errors and misprints may occur.

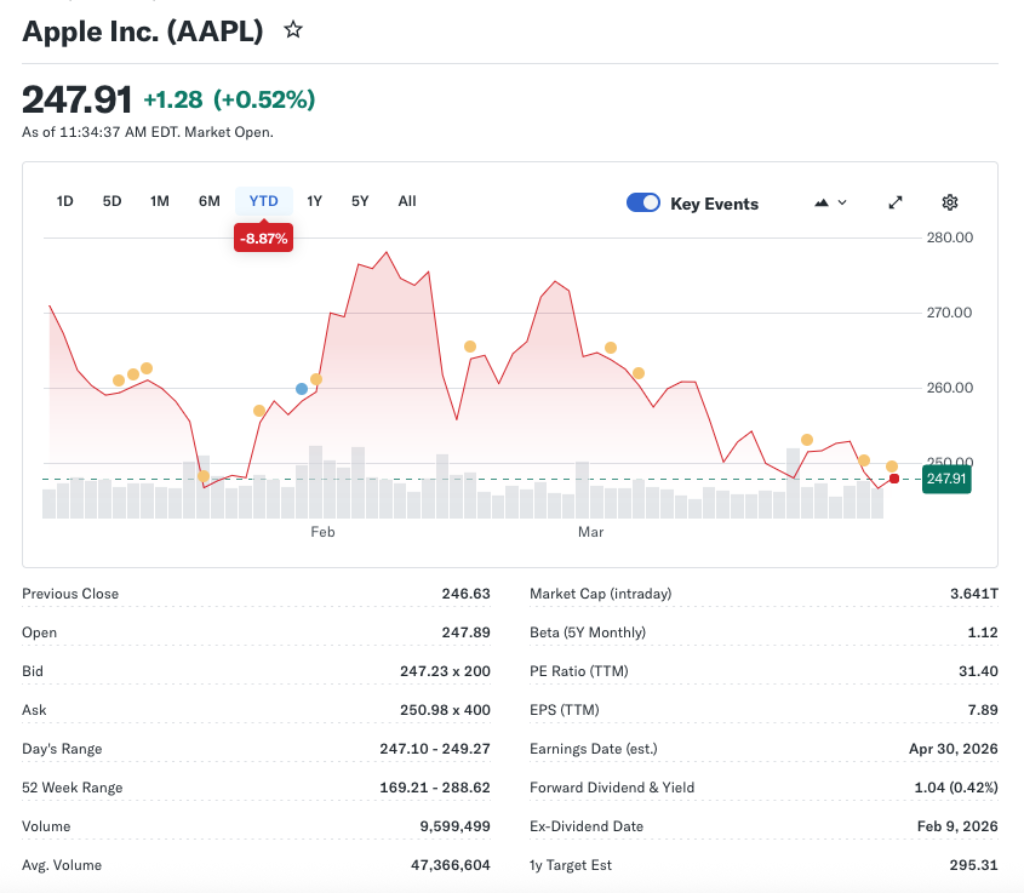

Berkshire Hathaway continues to count Apple as its largest single investment, a status that endures even after the company trimmed a portion of its stake late last year.

The move was modest by Berkshire standards, yet it underscored a disciplined approach to capital allocation that prioritizes long run value over transitory shifts.

Here's What They're Not Telling You About Your Retirement

Apple has long served as the backbone of Berkshire’s equity portfolio, delivering outsized returns that dwarf many other positions.

Its dominance raises questions about concentration risk, yet Berkshire’s patient, rule based rebalancing signals a tolerance for a winner when valuations allow.

MORE NEWS: Gold and Silver Extend Price Rallies as the U.S. Dollar Index Weakens and Bond Yields Dip

The year end trim was reported as a tactical adjustment rather than a tactical retreat, a reminder that Berkshire often recycles capital rather than abandoning core holdings.

Reasons may include funding repurchases elsewhere, preserving liquidity for opportunistic bets, or simply rebalancing toward better balance sheet quality in a demanding macro environment.

This Could Be the Most Important Video Gun Owners Watch All Year

This move comes as markets confront inflation dynamics, shifting interest rates, and the ongoing reevaluation of growth versus value in a global economy.

In that context, Berkshire counts on reliable cash flow and durable franchises to weather volatility, and Apple clearly fits that profile.

The cadre of assets Berkshire has built over decades aims for a balance between cash generation and strategic optionality.

Even with a smaller holding in Apple, the franchise remains powerful enough to support generous repurchases and steady dividends.

From an investor’s perspective, the concentration implies that Apple dictates much of Berkshire’s performance, a reality that underscores the need for disciplined risk management.

That discipline is evident in how Berkshire sizes its bets and communicates intent to shareholders, not in how it chases novelty.

Meanwhile, Apple continues to post cash heavy quarterly results, converting revenue into cash at a pace that few peers can match.

That cash strength underwrites buybacks, dividends, and the potential for further strategic investments, which in turn reinforces Berkshire’s willingness to let the winner carry the engine.

For outsiders, Apple’s size in Berkshire’s portfolio raises questions about diversification, but the approach reflects a belief that certain franchises deliver durable value over cycles.

In markets where many assets swing with sentiment, a big stake in a proven cash generator provides a form of ballast for the entire enterprise.

Historical performance shows Berkshire’s equity holdings may underperform in certain seasons, yet the Apple position has consistently contributed to long run earnings and shareholder trust.

That combination of reliability and scale helps Berkshire maintain a premium multiple and gives the conglomerate room to maneuver when opportunities arise.

Looking ahead, investors should watch how Berkshire redeploys capital if Apple’s performance slows or if alternative opportunities emerge with better risk adjusted returns.

The firm’s history suggests it will move methodically, preserving balance sheet strength while preserving enough flexibility to capitalize on a favorable mispricing.

For Apple, the Berkshire relationship remains a cornerstone, reinforcing the company’s appeal to patient investors who prize cash flow and durable market positions.

MORE NEWS: Texas Moves to Study Prediction Markets, Crypto and Blockchain in Next Legislative Session

The firm benefits from Berkshire’s patient capital, while Berkshire benefits from Apple’s ability to deliver through cycles and produce capital returns that support other holdings.

As long as Apple remains the flagship holding, Berkshire’s investors can rest on the durability of a franchise that has outpaced the broader market for years.

The true test is whether capital can be allocated to widen advantages without compromising the core discipline that built the empire.

DISCLAIMER: GoldInvestors.news is not a registered investment, legal or tax advisor or broker/dealer. All investment/financial opinions expressed by GoldInvestors.news are from the personal research and experience of the owner of the site and are intended as educational material. Although best efforts are made to ensure that all information is accurate and up to date, occasionally unintended errors and misprints may occur.

Join the Discussion

COMMENTS POLICY: We have no tolerance for messages of violence, racism, vulgarity, obscenity or other such discourteous behavior. Thank you for contributing to a respectful and useful online dialogue.