DISCLAIMER: GoldInvestors.news is not a registered investment, legal or tax advisor or broker/dealer. All investment/financial opinions expressed by GoldInvestors.news are from the personal research and experience of the owner of the site and are intended as educational material. Although best efforts are made to ensure that all information is accurate and up to date, occasionally unintended errors and misprints may occur.

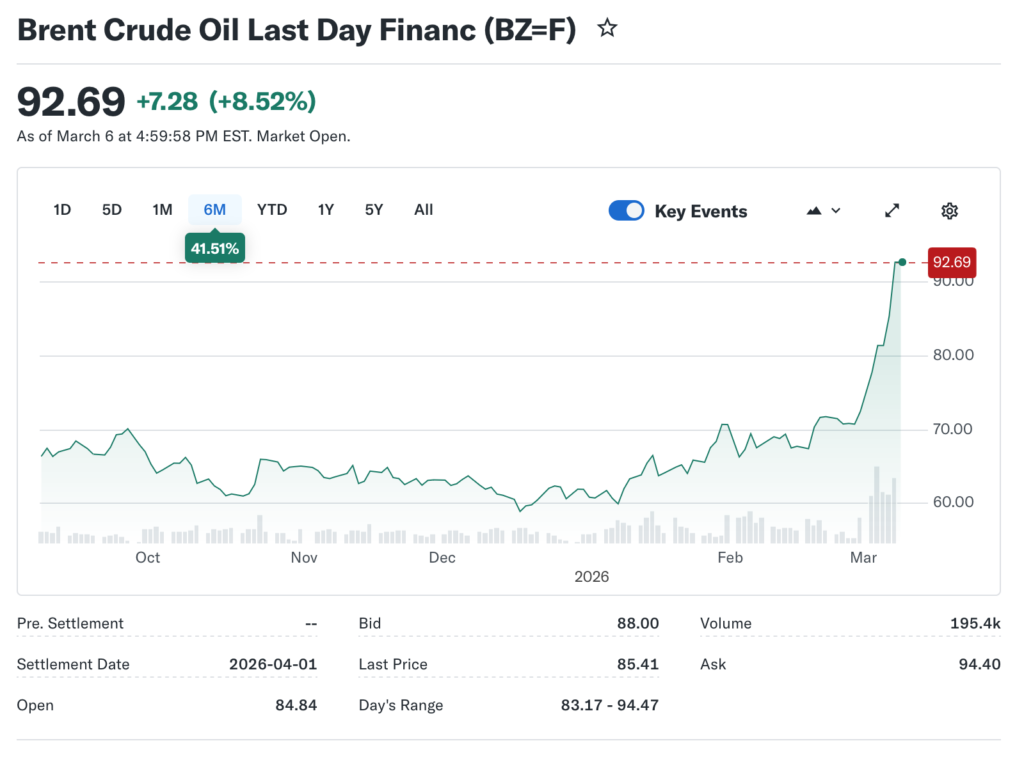

A team of Goldman Sachs' Asia Pacific energy analysts recently laid out a scenario that could recalibrate the earnings trajectory for China's top oil incumbents. They argue that if Brent crude maintains a firm rally amid persistent Middle East tensions, two of the three state backed giants may see stronger profitability.

The three leaders in Chinese oil are CNPC's PetroChina, Sinopec, and CNOOC, each with different exposure to international crude and downstream refining. The bank's analysts argue that a sustained Brent lift would lift export margins and boost top line results for players with meaningful foreign sales and sizable refining throughput.

From a conservative investment perspective, the logic is straightforward: higher crude prices tend to lift upstream revenues and improve refining economics, even in a market where domestic demand dynamics are fragile. But the benefit is not automatic, since currency movements, hedges, and cost structures complicate the outcome.

For the Chinese majors, the degree of benefit depends on how much of their output is tied to international benchmarks and how much of their refining capacity can capture global price signals. That exposure varies by company and by product mix.

Here's What They're Not Telling You About Your Retirement

In practice, CNPC and Sinopec operate large downstream networks that can profit from product price changes and arbitrage in international markets, while CNOOC retains more exposure to upstream pricing and offshore production. The result is a mosaic of earnings drivers across the trio.

The implications for investors are nuanced. A Brent rally often comes with higher volatility and may affect credit metrics differently across the majors.

Goldman Sachs cautions that the positive effects hinge on a price regime that remains supportive without triggering demand destruction or policy distortions from Beijing. In other words, the upside is conditional on sustainable energy prices and prudent macro policy.

This Could Be the Most Important Video Gun Owners Watch All Year

The broader macro backdrop remains delicate, with global growth signals uneven and inflation dynamics stubborn. That complexity can mute some upside from a crude run, particularly if the energy transition shifts emphasis away from fossil fuels in the medium term.

Investors seeking exposure to energy equities should weigh hedging strategies and the potential for divergence between upstream and downstream earnings across the Chinese majors. The Goldman call provides a framework for evaluating how Brent movements could reshape earnings mix and equity valuations.

Saudi Arabia and other Gulf producers have used Brent strength to justify production discipline, a practice that tends to support market prices. That dynamic can reinforce the price backdrop that benefits the Chinese majors when Brent holds gains.

Within China, the state maintains a delicate balance between supporting industrial growth and managing a currency sensitive to energy shocks. Policy responses to energy price swings can alter the translation of crude gains into corporate profits.

As always in commodity markets, the drivers are global and unpredictable, yet the Goldman call offers a disciplined framework for assessing how a Brent lift may influence the earnings mix of the country’s big oil players. For investors seeking excess return or safe exposure, the story remains a reminder that headlines in the Middle East can reverberate through Shanghai trading floors.

DISCLAIMER: GoldInvestors.news is not a registered investment, legal or tax advisor or broker/dealer. All investment/financial opinions expressed by GoldInvestors.news are from the personal research and experience of the owner of the site and are intended as educational material. Although best efforts are made to ensure that all information is accurate and up to date, occasionally unintended errors and misprints may occur.

Join the Discussion

COMMENTS POLICY: We have no tolerance for messages of violence, racism, vulgarity, obscenity or other such discourteous behavior. Thank you for contributing to a respectful and useful online dialogue.