DISCLAIMER: GoldInvestors.news is not a registered investment, legal or tax advisor or broker/dealer. All investment/financial opinions expressed by GoldInvestors.news are from the personal research and experience of the owner of the site and are intended as educational material. Although best efforts are made to ensure that all information is accurate and up to date, occasionally unintended errors and misprints may occur.

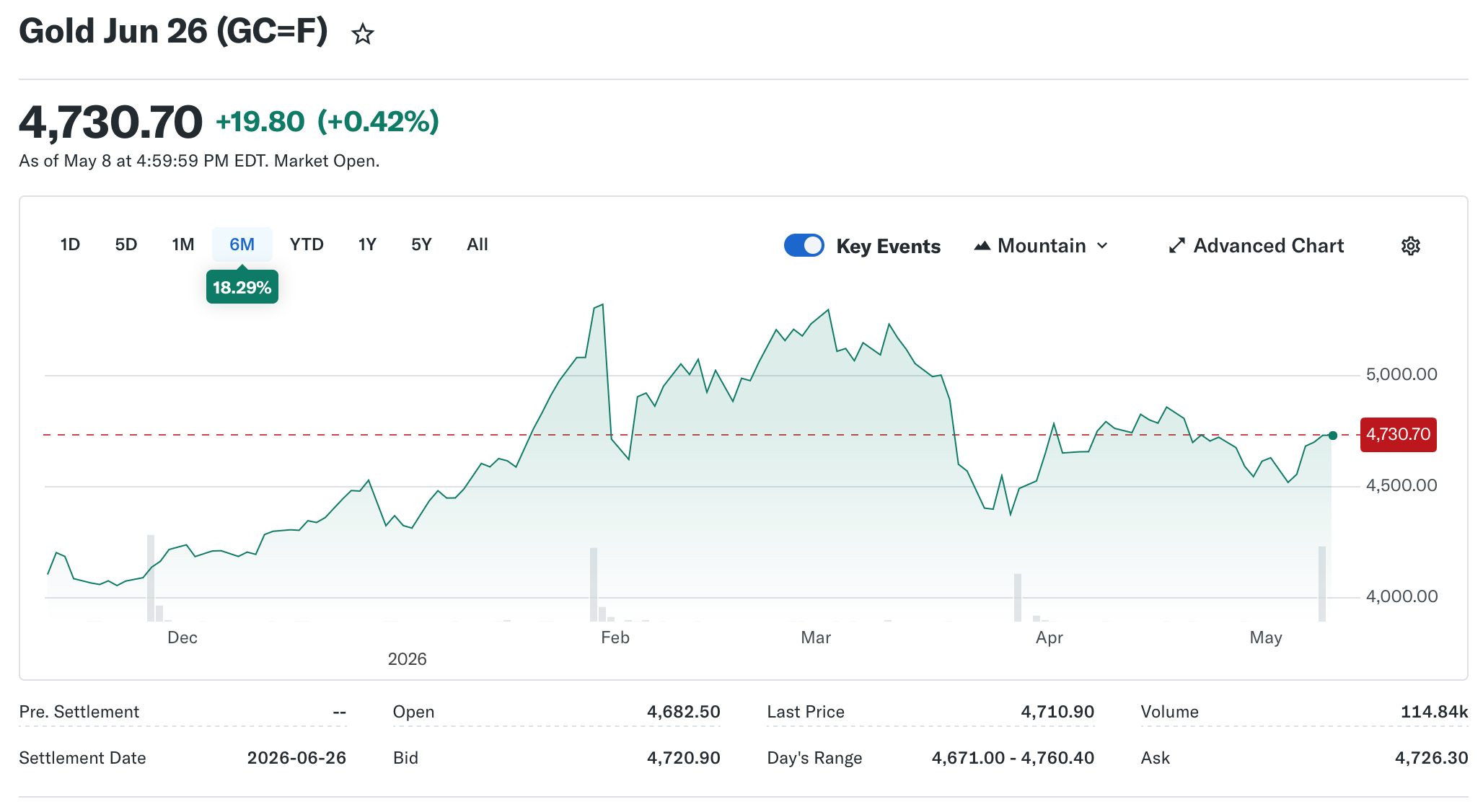

Gold prices may be consolidating after a massive run higher, but global central banks aren’t easing off the gas.

The latest trend shows they remain determined to accumulate bullion, particularly when prices dip.

Despite a few headline‑grabbing sales, the broader direction among policymakers remains one of quiet, persistent buying — a signal that gold’s role as a strategic monetary asset is far from fading.

According to new figures from the World Gold Council, central banks collectively sold a net 30 tonnes of gold in March, a statistic that at first glance might suggest waning interest.

Here's What They're Not Telling You About Your Retirement

However, most of that selling came from Turkey and Russia, two nations confronting unique domestic and geopolitical pressures. Strip those outliers away, and the underlying story points to a continued structural appetite for physical gold.

Countries like Poland, Uzbekistan, and Kazakhstan all added to their holdings during the same period, while China continued its now‑famous accumulation run that has stretched for 18 consecutive months.

Those purchases have been large enough to offset much of the global selling, reinforcing that the world’s largest emerging powers continue to view gold not merely as a commodity, but as a financial insurance policy against monetary instability.

China’s gold accumulation speaks volumes. The People’s Bank of China purchased 8 tonnes of gold in March alone, the biggest monthly increase since December 2024. Prices remain well below their January 2026 record, indicating that Beijing is strategically buying on dips, not chasing rallies.

This Could Be the Most Important Video Gun Owners Watch All Year

In effect, China’s accumulation pattern demonstrates that its approach is tethered to long‑term positioning, not short‑term speculation.

Even more telling is the relatively small portion that gold occupies within global foreign exchange reserves.

Gold accounts for roughly 15 percent of total reserve assets worldwide, according to World Gold Council data. That means the metal’s share remains far below potential, leaving significant headroom for further buying as countries diversify away from dollar‑based holdings.

Kosovo’s recent first‑ever decision to acquire gold shows the trend is broadening.

Smaller nations, long insulated from major reserve diversification plays, are now following the example of larger economies that are positioning gold as a hedge against currency and policy risk.

When a tiny newcomer like Kosovo steps in, it signifies that faith in global fiat structures is thinning even among peripheral economies.

The global shift toward gold accumulation has structural implications. Analysts increasingly observe that official sector demand has grown less sensitive to price. In other words, central banks are no longer waiting for gold to become “cheap” before buying.

Instead, they see it as a core reserve asset that protects purchasing power over time, regardless of market swings. This steady approach has planted a firm floor beneath bullion prices even during periods of volatility.

For investors watching the metal, that is a crucial development. Speculators and ETF flows may still dictate short‑term moves, but the foundation of demand now rests on sovereign buyers with deep pockets and long horizons.

That kind of backing is fundamentally different from retail enthusiasm or hedge‑fund momentum trades. It stabilizes the market from underneath rather than chasing it from above.

Market strategists argue that this official buying has established a “structural bid” in the market, discouraging deeper sell‑offs. Each time the price of gold dips, central banks appear ready to take advantage. The result is a market that consolidates instead of collapsing, even in the face of higher bond yields and a broadly stronger U.S. dollar.

MORE NEWS: SpaceX Rockets Into Nasdaq-100 as Fast-Tracked Inclusion Sparks Massive ETF Buying Frenzy

None of this guarantees smooth sailing. Gold could still face pressure if real yields climb or if global growth surprises to the upside, drawing flows back into risk assets.

Yet the central bank accumulation pattern suggests that any correction will be met quickly with official demand, cushioning downside risks for longer‑term holders.

Geopolitical tensions are also likely to support ongoing purchases.

The fragmentation of global trade, increasing sanctions activity, and distrust of dollar dominance have all pushed central bankers to think in terms of legacy preservation instead of quarterly metrics.

A growing number of national treasuries appear to prefer the surety of gold over the promises of paper.

At a time when many fiat currencies are facing credibility challenges, gold stands as the ultimate reserve asset that requires no counterparty.

Central banks seem to understand that lesson clearly, even as many private investors remain distracted by tech bubbles and complex financial engineering. Their actions speak louder than policy statements.

As long as central banks keep adding to their vaults, the fundamental case for gold remains intact.

The metal’s price may fluctuate with market cycles, but its strategic importance within global reserves is only trending upward. That quiet, steady buying is likely one of the most powerful, underappreciated forces keeping gold resilient through 2026 and beyond.

DISCLAIMER: GoldInvestors.news is not a registered investment, legal or tax advisor or broker/dealer. All investment/financial opinions expressed by GoldInvestors.news are from the personal research and experience of the owner of the site and are intended as educational material. Although best efforts are made to ensure that all information is accurate and up to date, occasionally unintended errors and misprints may occur.

Join the Discussion

COMMENTS POLICY: We have no tolerance for messages of violence, racism, vulgarity, obscenity or other such discourteous behavior. Thank you for contributing to a respectful and useful online dialogue.