DISCLAIMER: GoldInvestors.news is not a registered investment, legal or tax advisor or broker/dealer. All investment/financial opinions expressed by GoldInvestors.news are from the personal research and experience of the owner of the site and are intended as educational material. Although best efforts are made to ensure that all information is accurate and up to date, occasionally unintended errors and misprints may occur.

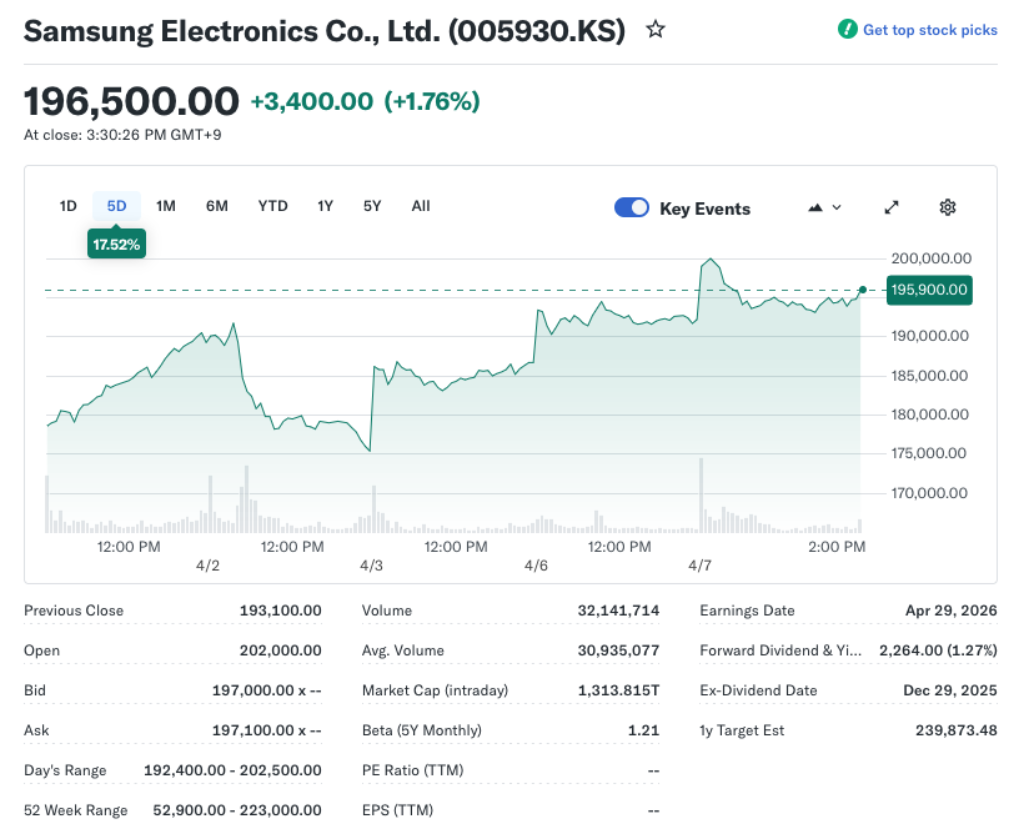

Samsung Electronics is trading higher after the company forecast a record breaking quarter driven by the surge in AI hardware demand.

Intraday, the stock rose as much as 4.8 percent before settling about 1.8 percent higher as traders weighed the implications for earnings, capital allocation and the broader tech cycle.

Management projected a record breaking quarter as demand for AI accelerators, servers and advanced memory chips remains robust across data centers, cloud providers and enterprise infrastructure, reflecting persistent capex commitments.

The market is interpreting that guidance as a signal that an extended cycle of tech spending is unfolding, which could translate into improved margins and stronger free cash flow for the year.

Here's What They're Not Telling You About Your Retirement

Analysts have argued the AI hardware wave is reshaping the semiconductor landscape and lifting margins for integrated device makers that can scale production and manage supply better than less diversified peers.

The market reaction suggests investors expect a durable lift from higher capex in data centers and cloud workloads, even as some doubts linger about potential inflationary pressure and supply chain bottlenecks.

Samsung's exposure to memory and logic devices positions it to benefit from rising demand for faster memory, higher bandwidth components and efficient processing, all of which are essential to sustaining AI workloads.

This Could Be the Most Important Video Gun Owners Watch All Year

At the same time, the company benefits from its integrated supply chain, global footprint and scale, which can translate into better pricing power and capital efficiency in a volatile cycle.

Profitability expectations hinge on mix, yield management and the ability to safeguard margins amid competitive pressure from other memory and foundry suppliers.

The reported numbers are likely to reflect strength in both device sales and component exports, which helps explain the quick market reaction and the perception that earnings power remains intact.

Yet the AI driven upcycle carries risks, including potential volatility in memory prices, shifts in capex timing and the possibility of a sharp correction if demand cools.

MORE NEWS: SpaceX Poised for Historic $75 Billion IPO as Wall Street Braces for Record-Breaking Debut

For now, discipline around investment in new capacity and product mix may be decisive in sustaining the upgrade in earnings, which requires careful management of capital expenditure and pricing strategy.

Global demand for AI hardware remains robust, and Samsung's role as a supplier to cloud providers gives it leverage in negotiations around pricing, lead times and contract terms.

That leverage will depend on the company’s ability to secure supply of substrates and keep foundry capacity flowing, which are ongoing challenges for the sector and beyond the company's direct control.

Investors are pricing in a favorable longer term outlook that includes heavy capital spending from major technology players and a continued tilt toward memory and logic upgrades.

The initial reaction is to interpret the forecast as evidence that the AI investment cycle has staying power and that Samsung sits at the center of that cycle, ready to benefit from incremental capacity additions.

Compared with peers, Samsung's integrated model and breadth across memory, display and smartphone components may provide greater ballast in a cyclical upturn despite ongoing competition and pricing erosion in certain sub segments.

The company has shown a capacity to translate product strength into earnings growth when AI demand accelerates, but investors still require visible evidence of sustained pricing power.

Valuation remains a key question for many investors as price gains test the balance between opportunity and risk amid a raised rate environment and evolving supply chain dynamics. Despite that, the earnings trajectory implied by the guidance could justify a higher multiple if the AI cycle proves sustainable and if Samsung can translate capacity into consistent cash generation.

Longer term investors will want to see how Samsung sustains pricing power and product mix through a potential cycle shift driven by technology upgrades and customer onboarding in new markets.

That outcome will depend on competitive dynamics among memory suppliers, foundry customers and the pace of AI hardware replacement, all of which can matter more than short term sentiment.

Samsung appears poised to capitalize on a multi quarter run in AI hardware demand by aligning product roadmaps with customer needs and disciplined capital planning.

Whether the gains endure will rest on execution and the broader demand environment across data centers and consumer devices, a combination that demands prudence and steady stewardship from management.

DISCLAIMER: GoldInvestors.news is not a registered investment, legal or tax advisor or broker/dealer. All investment/financial opinions expressed by GoldInvestors.news are from the personal research and experience of the owner of the site and are intended as educational material. Although best efforts are made to ensure that all information is accurate and up to date, occasionally unintended errors and misprints may occur.

Join the Discussion

COMMENTS POLICY: We have no tolerance for messages of violence, racism, vulgarity, obscenity or other such discourteous behavior. Thank you for contributing to a respectful and useful online dialogue.